At this time, I would like to discuss mobile payment systems like Apple Pay, Google Pay or Samsung Pay, These systems are typically associated with payments made via mobile devices, rather than card, check or cash. Mobile payments has been slowly adopted since year 2000, and as of now you can find plenty of merchants accepting mobile payments. It is worth to mention that mobile payments are not limited to mobile devices only (they may also be made using contactless cards, digital wallets, wearable devices, etc.), but right now I wanted to focus on three systems from major commercial providers mentioned above.

First and the most important aspect of these systems is that they do not replace fiat currency, cash or credit cards: mobile payment just provide a convenient and secure way to use them. One or more debit or credit card must be linked to the account, in order to deposit, withdraw or send money. As you may guess, card balances are being processed in the way identical to traditional usage. Also operations can be made in digital cash (such as Apple Pay Cash), which are always supported by traditional banks. While most credit or debit cards can be used across the border, digital cash so far is limited to operations within one country.

Technically speaking, there are at least two main functions common across mobile payment systems:

- digital wallet

- in-store payment

Digital wallets are not limited to Apple, Google or Samsung: there are plenty of other providers such as PayPal, Square, Wenmo for example. Each service operates through the website or application on mobile device and requires debit or credit card to be linked to account. It allows sending money to other person using email address rather than bank account/routing number opposite to ACH or wire transfer. While this is definitely a better way for instant payments, I am still not convinced in their unique value in helping people to earn rather than spend their money. However, one system definitely has an edge and it is Google Pay. With Google, there is always a link between email and wallet account. Moreover, one person may have more than one account and send money between these accounts. It becomes handy, when dealing with interest checking accounts which require certain amount of money to be deposited or withdrawn every month in order to qualify for higher better rate. In this way, digital transactions actually replaces in-store or online purchases and helps to earn higher interest.

Other important function is in-store payments. While digital wallets were around for many years, in-store payment is a relatively new function limited to major providers of mobile operating systems and devices such as Apple, Google and Samsung. It requires support by merchant payment terminal, as well as use of certain mobile or wearable device. Lately most stores in US and across the world installed equipment for contactless payments, which include mobile in-store payments. In order to have impression about the availability of this technology, please check the data: as of November 2017 Apple Pay had support in 25 countries, Google Pay in 17 countries and Samsung Pay in 21 countries. The coverage is growing rapidly.

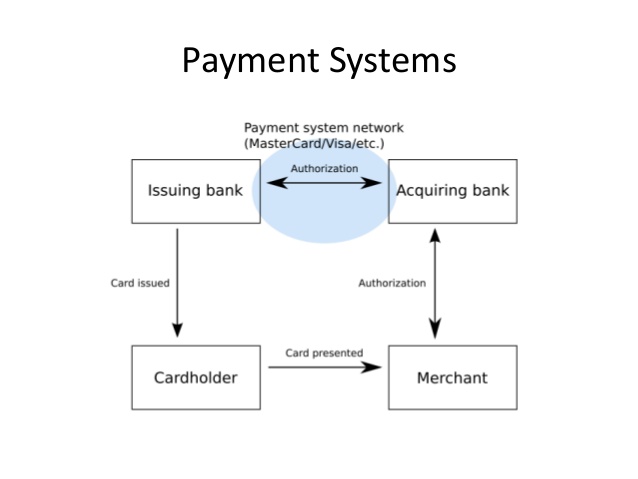

But in addition to merchant terminal support, there is a need for certain device in order to use the service. The list of supported devices is available: basically the device must have NFC (Near Field Communication) chip built into it. But while Google Pay can work with virtually any device with NFC running Android OS, Apple and Samsung Pay are limited to the devices made by respective companies. In order to understand the benefits, it is important to know how traditional payment system with credit or debit card works.

One important step is when merchant’s device read the card data and send it to acquiring bank for authorization. Therefore, merchant has all data which potentially can be vulnerable to theft. With mobile payments using NFC, the data are transferred using one-time secure dynamic code encrypted to hide credit or debit card information from merchant. It is also important that device can operate in offline mode during in-store purchase (no mobile data or wifi connection) to prevent actual card data to be sent somewhere by malicious software. This code is directly transferred to the bank and payment system network for further decoding and processing the payment. The decoding method is unique for each device and card, and established during the initial setup of payment system on that specific device. At this time, data connection is required.

One other important aspect of mobile payment systems is in their difference. While Apple Pay can function for in-store purchases completely offline for indefinite time, Google and Samsung Pay provide tokens for 10 in-store offline purchases. After that, device must be connected to Internet in order to receive another 10 tokens. Also, Samsung Pay can work not just with merchant terminals equipped with NFC reader, but with magnetic stripe as well. This may be important for US store chains, which did not install NFC support yet. Another aspect is security: Apple and Samsung systems seems more secure than Google, just because payment support built directly into their own devices.

It is easy to set up and use the system: install digital wallet application from online store (on Apple or Samsung devices, application is available by default), establish account (typically it is possible to use existing account for iTunes purchases or Google Wallet for example) and link appropriate cards. Although I find it hard to deal with Google Pay on LG G2 device upgraded to Android 5.0.2: application determined that some software on the device has been altered and refused to link a card. But it was a seamless experience with iPhone 6 Plus. When making purchase in store, it is required to launch wallet application (in most cases), choose appropriate card (or use a default one) and then hold device close to the merchant terminal without touching it, until operation is indicated as complete. Finger recognition feature enabled on compatible devices is extremely handy just in case someone else gain access to the device and credit cards stored in digital wallet.

Besides the secure data transfer and obviously no need to carry credit or debit cards, what are other benefits of these systems? I found there are important advantages when you live outside of US for extended time and keep using credit cards issued in US. Lately in multiple cases US citizens were not able to open bank accounts in foreign countries due to the strict international regulations about money laundering, so this opportunity can be vitally important. In this case, actual card is not required for in-store purchases: all you need to know is a card number and expiration date, in order to link it with payment system. By that reason, it is possible to avoid a hassle of sending physical cards overseas. Also there could be multiple points of sale abroad where certain types of US issued credit cards are not accepted. But payment system effectively removes the direct communication between merchant and credit card: support for Apple, Google or Samsung Pay is just a single requirement in this case, regardless of the card being used.

What is a future of mobile payment systems? All these latest and greatest mobile devices with support for NFC payment are quite expensive: many people just can not afford them. Moreover, there are still people without a smartphone. Also, online payments support is currently limited. On my opinion, payments are likely to be made using cheap wearable devices easily available to everyone. They may be even implanted into the human body. No need to send physical card, no need to carry it in real wallet. And potentially it could be a great platform for transition to virtual currency.